US Dollar surges to eleven month high on Trump effect

- Go back to blog home

- Latest

15 November 2016

Senior Market Analyst at Ebury. Providing expert currency analysis so small and mid-sized businesses can effectively navigate international markets.

The US Dollar rose sharply for the fourth straight session against its major peers on Monday.

G10 and emerging market currencies alike lost ground, with very few currencies spared from yesterday’s sell-off. The Euro plunged to its weakest position against the Dollar since early January this year, while the Pound reversed some of its recent gains to end the day half a percent lower.

The single currency has fared particularly poorly since Trump’s election victory, which has heightened the risk of an increase in support for anti-establishment movements within Europe.

The next event risk for the Euro will be the Italian constitutional referendum on 4 December. Support for the ‘No’ vote on a number of widespread political reforms has increased in the past few weeks and is now marginally ahead. A defeat for Italy’s Prime Minister Matteo Renzi would open up the possibility of a new national election and no doubt increase support for the country’s Eurosceptic Five Star Movement Party.

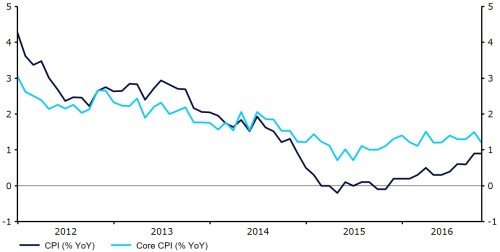

Investors are likely to temporarily turn their attention away from political developments today, and focus on a string of economic announcements in the major economies. Inflation in the UK came in below expectations at 0.9% in October (Figure 1), with this morning’s Eurozone GDP data unrevised at 0.3%.

Figure 1: UK Inflation Rate (2012 – 2016)

The latest retail sales figures in the US this afternoon is also likely to prove a market mover, although even a very weak number is unlikely to derail the chances of a Federal Reserve rate hike next month which currently stands at around 85%. Federal Reserve Chair Janet Yellen is expected to reemphasis the need for higher rates in the US when she speaks in front of Congress on Thursday afternoon.

Major currencies in detail:

GBP

Sterling finally succumbed to the post-election Dollar strength yesterday, falling by 0.3% against the greenback.

The Pound’s rally ran out of steam yesterday, having last week emerged as an unlikely benefiter of the Donald Trump election victory. An increased risk of contagion for anti-establishment movements, particularly in Europe, has heightened since the Trump’s election and has temporarily shifted the political risk premium away from the UK. This, coupled with the likely delay in the triggering of Article 50, should keep Sterling well supported in the coming days.

The latest labour report on Wednesday and retail sales on Thursday mark a busy week in the UK.

EUR

The Euro sank for another day on Monday, with a broadly stronger US Dollar sending the single currency 0.5% lower.

The Euro took little notice of a slightly more encouraging set of industrial production data for September. Output rose by 1.2% in the year to September, falling by a slightly better-than-expected 0.8% in the month. This follows a general improvement in the latest business activity and inflation numbers, which have fuelled faint hopes of an economic recovery in the Euro-area.

Third quarter GDP data and the latest ZEW economic confidence index failed to material shift the Euro this morning. Attention remains firmly on political developments in Europe ahead of the Italian Constitutional referendum.

USD

The US Dollar index rose above 100 for the first time in almost a year yesterday, rising by 0.4%.

In the absence of any additional economic news yesterday, the Dollar continued to be driven on growing expectations for the next interest rate hike by the Federal Reserve. We think Donald Trump’s plans to ramp up spending and cut taxes next year means there is now a reasonable argument to suggest that the Federal Reserve could hike rates at an even faster pace in 2017 than most analysts had originally envisaged.

Speeches from Federal Reserve members Rosengren, Bullard and in particular Janet Yellen this week are also likely to shed more light on the Fed’s rate hike plans for the coming months.

Receive these market updates via email

SHARE