Dollar firms on signs of narrowing US trade deficit

- Go back to blog home

- Latest

5 April 2017

Senior Market Analyst at Ebury. Providing expert currency analysis so small and mid-sized businesses can effectively navigate international markets.

The US Dollar rose against its major peers on Tuesday after the release of the latest trade balance data out of the US suggested that growth in the world’s largest economy may be set to accelerate in the first quarter of the year.

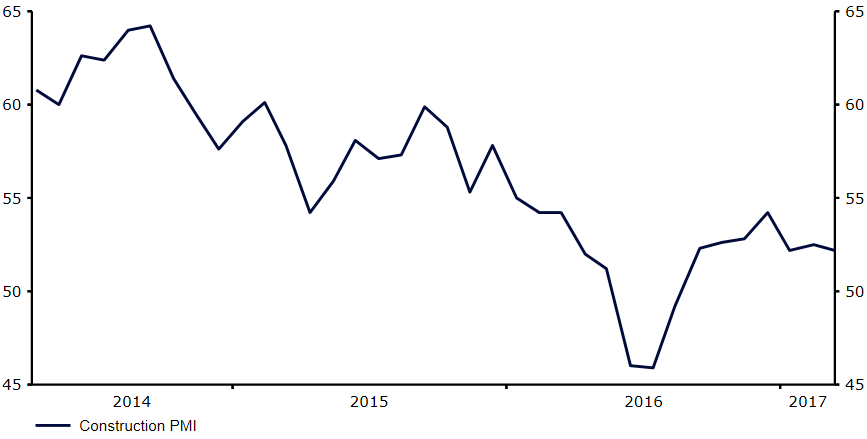

Earlier in the session, Sterling fell after the monthly construction PMI in the UK came in less than expected, boding poorly for this morning’s services index. The construction index declined to 52.2 from 52.5 (Figure 1), adding to the recent signs that the UK economy may be losing steam ahead of the likely protracted period of Brexit negotiations. This morning’s services index will take on added importance given the sector’s large contribution to overall GDP. Any reading less than the 53.1 consensus could prove a significant negative for the Pound today.

Figure 1: UK Construction PMI (2014 – 2017)

Meanwhile, pressure continued to mount on South African President Jacob Zuma to stand down following his decision to orchestrate a massive reshuffle of his cabinet last week. The Rand has plunged by over 10% in the past week on the back of the news to its lowest level since the beginning of December.

This evening we’ll also have the release of the Federal Reserve’s meeting minutes from its March meeting. Policymakers in the US kept their expectations for future rate hikes unchanged from the December meeting. The minutes could give the market additional clues as to the likelihood that the Fed will hike rates more aggressively in 2017 than the market is currently pricing in.

Major currencies in detail

GBP

Expectations for higher interest rates in the UK before the end of the year have taken a slight blow in the past couple of days. Yesterday’s construction PMI miss adds to a similarly downbeat reading in Monday’s manufacturing index. We’ll get the first piece of hard data on the UK’s performance in the first quarter when the latest GDP growth numbers are released at the end of the month.

This morning’s services PMI will be released at 9:30 UK time. Investors will also have one eye on Friday’s manufacturing and trade numbers.

EUR

The Euro was fairly range bound against its major peers on Tuesday, despite the release of a better-than-expected set of retail sales data.

Retail sales in the Eurozone accelerated for the second straight month, increasing by 1.8% in the year to February, comfortably above the 1.4% consensus. However, reaction to the news was fairly limited with investors giving more focus to events elsewhere.

The updated services PMI this morning is expected to remain unrevised from the initial flash estimate. The Euro is likely to be driven predominantly by the Federal Reserve minutes later this evening.

USD

News out of the US was fairly limited on Tuesday and even a live press conference from Donald Trump was not enough to significantly shift the Dollar.

Focus today will be on the FOMC minutes, set to be released at 19:00 UK time. In the meantime, the latest services PMI from Markit is expected to show a modest uptick on previous.

As always, Friday’s nonfarm payrolls report will likely prove a market mover. Consensus is for a reading around the 180,000 level, which would be enough to convince us higher interest rates are a strong possibility at one of the Fed’s next two meetings.

SHARE