Sterling soars after Davis fuels hope of ‘softer Brexit’

- Go back to blog home

- Latest

2 December 2016

Senior Market Analyst at Ebury. Providing expert currency analysis so small and mid-sized businesses can effectively navigate international markets.

The Pound rose sharply against both the Euro and the US Dollar on Thursday after Brexit secretary David Davis fuelled hope that Britain could retain access to the single market following its EU exit.

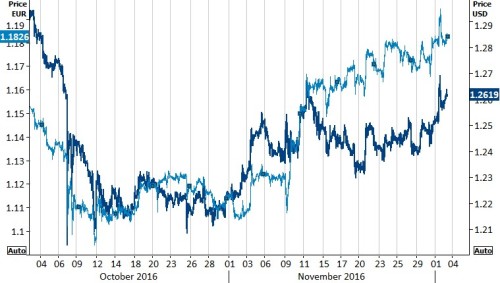

Sterling reacted very positively to the news, rallying to a 7 week high against the US Dollar and soaring to its highest level versus the Euro since the beginning of September (Figure 1).

Figure 1: GBP/USD & GBP/EUR (October ‘16 – December ‘16)

Focus today will be firmly on the monthly labour report in the US, including the crucial nonfarm payrolls number, widely regarded as the most important macroeconomic data release of the month. All signs point to a reasonably strong report in our view. This follows four decade low levels of jobless claims and an impressive ADP employment report released on Wednesday, which showed a significant uptick in private sector payrolls.

We think the bar is incredibly low for the Federal Reserve to hike interest rates in a couple of weeks’ time and think that even a very weak report today will do little to derail the chances of a hike when policy makers next meet on 14 December.

Among emerging markets yesterday, the Turkish Lira was sent crashing to a fresh record low against the US Dollar as political uncertainty and concerns over rising oil prices severely damaged sentiment towards the currency. The Mexican Peso also slipped by almost one percent against the US Dollar after the resignation of the country’s central bank governor.

Major currencies in detail

GBP

After initially spiking by more than one percent, Sterling retraced its gains to end the session 0.5% higher against the US Dollar.

Yesterday’s manufacturing PMI for November came in significantly below expectations, although investors gave it little attention as the Pound continues to be driven by political developments and nothing else. The PMI sank to 53.4 from a revised 54.2 in October, albeit still comfortably above the level of 50 that denotes expansion.

Chancellor Philip Hammond also quashed speculation that Scotland could gain a separate Brexit deal to the rest of the UK, claiming it was “not realistic”.

This morning’s construction PMI is unlikely to shift the Pound today with Sterling continuing to be driven almost exclusively by Brexit news.

EUR

The Euro continued to remain relatively range bound against the US Dollar yesterday and was little changed, finishing 0.3% higher.

Unemployment data on Thursday was resoundingly positive. The jobless rate in the currency bloc fell unexpectedly to 9.8% versus the 10% consensus, marking its lowest level in 7 years. The manufacturing PMI for November came in at a solid 53.7 following relatively encouraging performances in Italy and France.

Unconfirmed reports yesterday also suggested that ECB policymakers had no intention to announce a tapering of their QE programme any time soon.

With no major economic data releases in the Eurozone today, Euro traders will be firmly focusing on this afternoon’s nonfarm payrolls report in the US.

USD

The US Dollar index was stuck in a range on Thursday, although slipped overnight ahead of today’s nonfarm payrolls report, opening this morning 0.4% lower.

Federal Reserve member Robert Kaplan spoke again yesterday, reiterating his view that the Fed should remove its accommodative monetary policy stance in the near future.

Meanwhile, economic data was fairly mixed in the US on Thursday. The manufacturing PMI from ISM, seen by the Federal Reserve as one of the main economic releases in the month, crushed expectations in November. The index climbed to 53.2 from 51.9, largely due to an increase in new orders. Contrastingly, initial jobless claims rose unexpectedly to a five month high 268,000, having recently fallen to their lowest level in over 40 years.

Today’s nonfarm payrolls figure is forecast to come in around the 175,000 mark when released at 13:30 UK time today. Any number around or above consensus should provide decent support for the Dollar today.

Receive these market updates via email

SHARE