Dollar rally falters on weak US inflation data

- Go back to blog home

- Latest

18 April 2017

Chief Risk Officer at Ebury. Committed to mitigating FX risk through tailored strategies, detailed market insight, and FXFC forecasting for Bloomberg.

The holiday-shortened week nevertheless brought some significant economic news from the US.

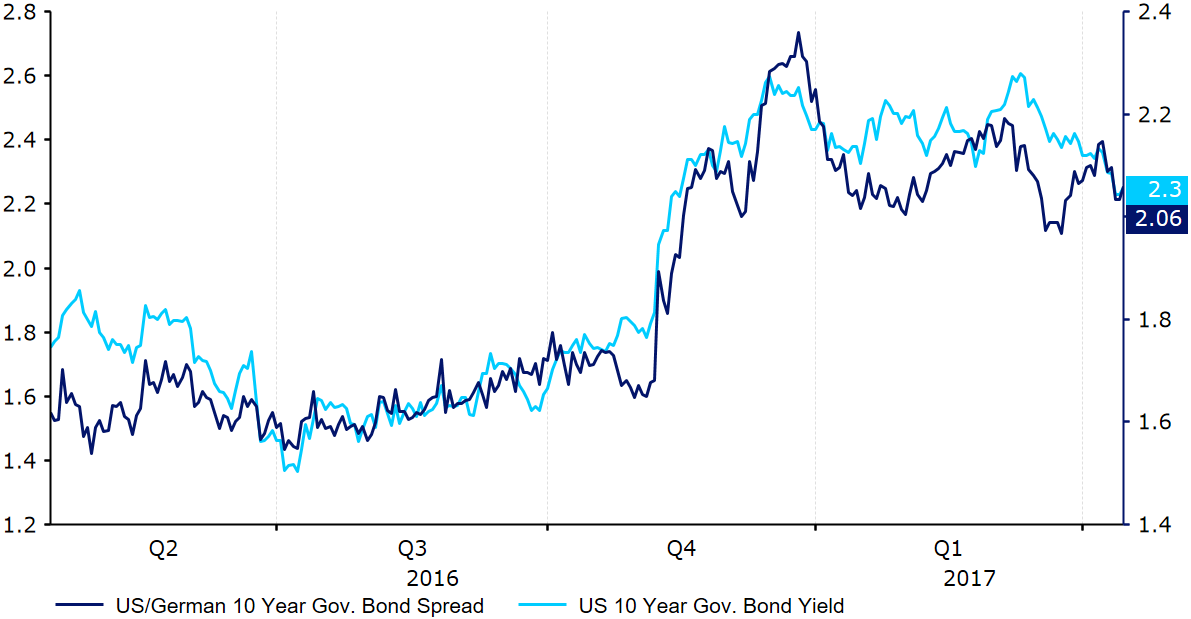

Figure 1: US 10 Year Government Bond Yield (2016 – 2017)

The common currency continues to struggle in the wake of uncertainty about the result of the French Presidential election.

Not surprisingly, the biggest beneficiary of lower US yields was the Yen, which rose against all other major currencies except the South African Rand, which experienced a dramatic rebound after the selloff sparked by the sacking of its respected Finance Minister the week before last.

Next week is shaping up to be a critical one for the Euro. On Wednesday there will be key speeches by ECB policymakers. Then on Friday we will get the flash PMI business activity indices, the most important leading indicator for the Eurozone economy as a whole. This will be followed on Sunday by the first round of the French Presidential election. The next few days could be quite volatile in FX markets.

Major currencies in detail

GBP

UK inflation and unemployment both stayed unchanged in March, much as the market has expected. Nevertheless, Sterling continued to rally against both the Euro and the US Dollar, as markets unwind their perhaps excessive pessimism of the last few months regarding Brexit negotiations.

The only data of note this week is retail sales, out on Friday. This is a volatile data point and the market impact is expected to be muted. Sterling will likely trade driven primarily by Eurozone news and geopolitical developments.

EUR

The Euro continues to lag most other G10 currencies, weighed down by uncertainty surrounding the French election as well as the dovish comments from ECB officials trying to talk down expectations for changes in ECB ultralax policy. The PMI indices of business activity are typically market-moving releases, but with the French election only two days later, it’s anyone’s guess how the markets will react. Consensus expectations are for a continuation of recent strength in the PMIs, which could make for some downside risks if the data pulled back after the sharp increase of the previous release.

The key event for the common currency will obviously take place on Sunday as the French go to the polls. The main risk in the first round will be a Melenchon-Le Pen pairing for the second, a low-probability but by no means an impossible event.

USD

Data out of the US last week was significantly weaker than expected. The volatile retail sales number showed the second consecutive month-on-month drop in March, although the less volatile indicator that excludes automobile sales and gasoline was still positive.

Harder to brush off was the large miss in inflation. The headline number came out at 2.4% on a year previous, 0.2% below expectations. More important was the core inflation number that excludes volatile food and energy components. The 0.1% contraction for the month of March was 0.3% below expectations. While a large part of the surprise can be ascribed to a one-off factor, the largest monthly decline in wireless telephone services in history, even excluding this the result would have been significantly below expectations.

We will be looking closely at next month’s release to see if the March data was an aberration or the beginning of a moderating trend in US price increases. For next week, however, there are almost no important news on tap in the US, so again geopolitical developments and French election polls will remain the key drivers for US Dollar trading against other G10 currency.

SHARE