Dollar soars on shock Trump election victory, as emerging market currencies sink

- Go back to blog home

- Latest

14 November 2016

Chief Risk Officer at Ebury. Committed to mitigating FX risk through tailored strategies, detailed market insight, and FXFC forecasting for Bloomberg.

Trump’s victory in the US Presidential elections completely overshadowed all economic and policy news last week.

However, early Wednesday morning financial markets took a closer look at the potential impact of a Trump presidency and had a complete change of heart. Stock markets and the Dollar at first stabilised, then rallied hard past their starting points on Tuesday to end the week solidly up.

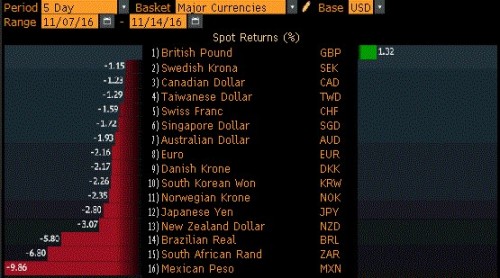

In the case of the Dollar, we saw the largest weekly rally since the financial crisis in 2008-2009. Only Sterling managed to rise against the US Dollar, in a move that appears entirely driven by the massive overhang of Pound shorts among professional traders.

Figure 1: Currency Performance vs. US Dollar (07/11/16 – 14/11/16)

Losses against the US Dollar were particularly brutal among key emerging market currencies. All the most liquid ones lost over 5% for the week. Unsurprisingly, the harshest punishment fell on the Mexican Peso, down around 10%.

The turnabout in FX market’s estimation of Trump was driven by the expectation of significant fiscal stimulus, from promised tax cuts and increased infrastructure spending. This additional stimulus comes as US wages are firming and US inflation starts to head up.

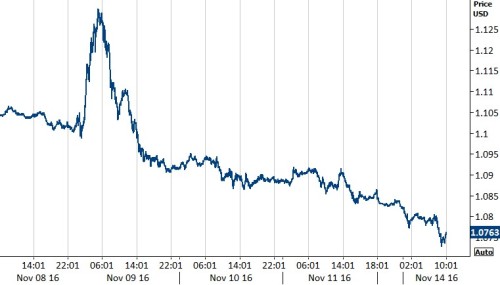

Figure 2: EUR/USD (08/11/2016 – 14/11/2016), Fed Vice chairman Fischer added fuel to the Dollar rally by sounding a hawkish note on Friday and implying that Trump’s victory did not substantially change the Fed’s view that higher rates are needed and driving the market’s expectation for a December hike to nearly 90%.

The move in US rates was also extraordinary. The 10 year Treasury yield rose by over 20% – the largest weekly move in at least 50 years.

What next?

G10 currencies

We strongly reaffirm our expectations for a stronger Dollar versus all of its G10 peers.

The combination of stronger growth, driven by significant fiscal stimulus injected into an economy near full employment, and higher interest rates is usually an irresistible magnet for portfolio flows and a very bullish signal for the currency. This is particularly true now, when most European currencies find themselves in the exact opposite situation, hampered by ultralow rates and sluggish growth.

Emerging market currencies

The prospects for emerging market currencies are less clear cut.

On one hand, the rise in US yields is generally negative. However, the strong reflationary impulse in the US should be quite supportive. Commodity prices should firm up as demand increases after recent significant cuts to production capacity.

Much will depend on each country’s exposure to Trump’s threatened restrictions on trade and its position as a net commodity importer or exporter.

Receive these market updates via email

SHARE