Currency markets remain rudderless as investors ponder next steps for Trump administration

- Go back to blog home

- Latest

27 March 2017

Chief Risk Officer at Ebury. Committed to mitigating FX risk through tailored strategies, detailed market insight, and FXFC forecasting for Bloomberg.

Markets spent last week in a holding pattern with all G10 currencies, save the Australian Dollar and the Yen, ending up less than 1% away from where they started.

The muted reaction to positive political and economic news out of the Eurozone indicates that those outcomes are mostly priced in by FX markets. Traders will be focused on the Trump administration’s ability to recover from last week’s defeat and enact tax cuts and, less likely this year, infrastructure spending.

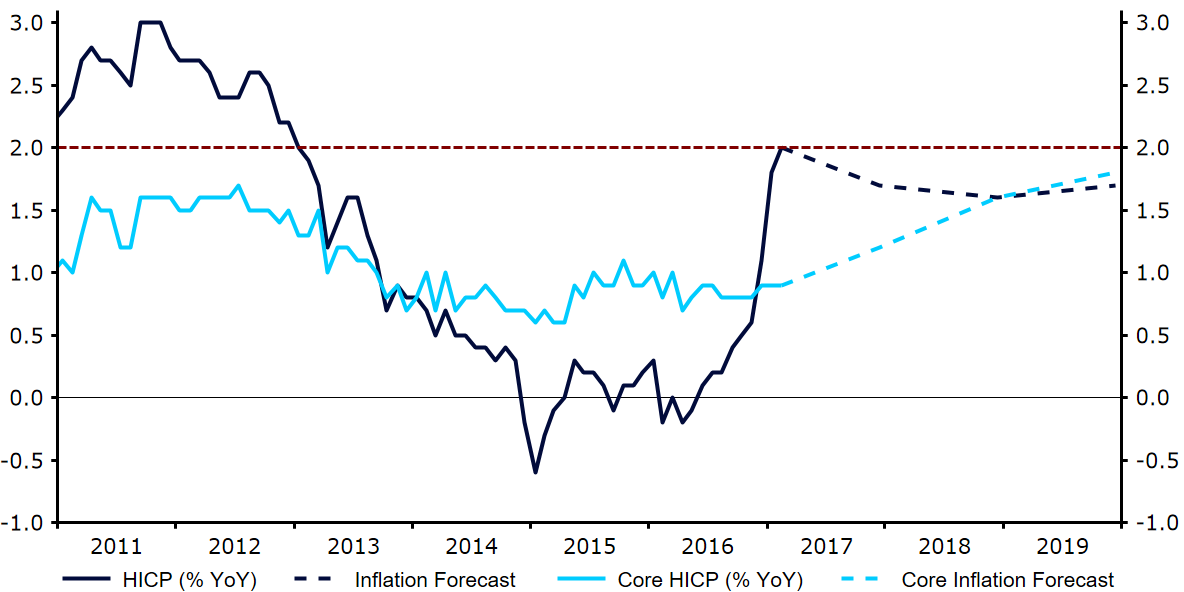

In addition to US politics, the focus next week will be on the Eurozone March inflation figure out on Friday. This will provide the first test of the ECB’s staff optimistic projections of a steady upward path in Eurozone core inflation back towards its target (Figure 1).

Figure 1: Eurozone Inflation Rate & ECB Projections (2011 – 2019)

Major currencies in detail

GBP

Last week’s upward surprise in UK inflation validates our view that interest rate markets are significantly underpricing the chance of a Bank of England hike before the end of 2017. Underlying inflation is already at 2%, the labour market is tight and we have yet to see all the pass through from currency weakness to higher import prices.

This mispricing, together with the “buy the rumour, sell the fact” dynamic that we are seeing around the triggering of Article 50, means that the recent Sterling rally probably has some legs, particularly against the Euro.

EUR

Markets largely ignored the higher-than-expected demand for ECB liquidity from Eurozone banks at its last Long Term Refinancing Operation (LTRO). Over €233 billion of cheap loans were snapped up, though it is far from clear that this reflects any heightened risk appetite on the part of Eurozone financial institutions. The PMI indices of business confidence were unambiguously positive, however, rising to a cycle high of 56.5 and consistent with acceleration of Eurozone growth to roughly the 2.5% level. The first quarter GDP numbers should be watched closely to see if business confidence actually translates into stronger investment.

Next week is very quiet in terms of Eurozone news, and we expect the common currency to take its cues from events elsewhere.

USD

After the disastrous failure of Republican efforts to “repeal and replace” Obama’s health care reform last week, the future of Trump’s promises to enact significant tax cuts and push through an infrastructure spending package is more uncertain than ever.

Since macroeconomic data is unlikely to surprise strongly to either side, currency markets will remain fixated on the US political calendar and, in particular, internal Republican tensions and wrangling over the upcoming tax reform and reduction proposals from the Trump administration.

SHARE