Clinton and Trump clash in first TV debate, Sterling edges higher

- Go back to blog home

- Latest

27 September 2016

Senior Market Analyst at Ebury. Providing expert currency analysis so small and mid-sized businesses can effectively navigate international markets.

The US Presidential Election took centre stage last night, with Hillary Clinton and Donald Trump engaging in the first in a series of TV debates ahead of November’s election.

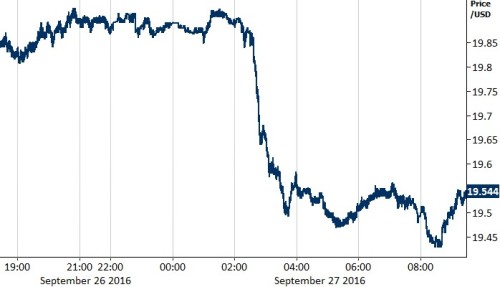

We look to the Mexican Peso, a currency that has been under heavy pressure since Donald Trump’s Presidential campaign began. The Peso surged almost 2% followed the debate (Figure 1), suggesting that investors viewed Clinton as the clear winner.

Figure 1: USD/MXN (26/09/2016 – 27/09/2016)

Sterling edged higher from its near five week low against the US Dollar on Monday, although gains were limited with investors remaining concerned about the likely timing of Article 50. The Pound has remained under pressure since Britain’s Foreign Secretary Boris Johnson last week warned the process was likely to be triggered early next year.

Earlier on Monday, the Japanese Yen edged ever closer to the psychological key support level of 100 to the US Dollar. This followed comments from the Bank of Japan Governor Haruhiko Kuroda that suggested the central bank is unlikely to increase its quantitative easing programme in the coming months.

Meanwhile among emerging markets, the Turkish Lira was one of the few currencies to end the day lower against the US Dollar following the decision of ratings agency Moody’s to cut the country’s rating to junk late last Friday.

Economic announcements out today are relatively thin on the ground. The preliminary services PMI in the US at 14:45 UK time and the latest consumer confidence index at 15:00 UK time will be the main data releases to look out for today.

Major currencies in detail:

GBP

A weaker US Dollar ahead of last night’s Election debate allowed the Pound to rebound from its multi-week lows, ending 0.3% higher against the Greenback.

There was limited news out of the UK yesterday, with Sterling largely driven by technical factors. Investors have begun eyeing up the next major support level of just below 1.29 to the US Dollar, since the Bank of England signalled that it could be ready to cut interest rates for the second time this year. The currency remains perilously close to the 31 year low reached following the Brexit vote.

Sterling will likely take more of a backseat this week with little in the way of major economic announcements out of the UK. Friday’s revised second quarter growth data is unlikely to rock the boat and is expected to remain unchanged.

EUR

The Euro edged 0.2% higher against the US Dollar yesterday, although was barely moved by comments from ECB President Mario Draghi.

Speaking in Brussels on Monday, Draghi reiterated the limitations of the ECB’s ultra-loose monetary policy in order to support both growth and inflation in the Eurozone. Draghi claimed low interest rates had long term side effects, instead calling for greater fiscal spending among governments within the Euro-area.

The Euro did, however, receive decent support from yesterday’s business sentiment indexes from IFO, all of which exceeded expectations. The main Business Climate Index rose to 109.5 from 106.2.

The mostly second-tier data, including Italian industrial output and German import prices, is not expected to be a big mover this morning. Mario Draghi will be the main focus for Euro traders when he makes his second public appearance of the week at an event in Berlin on Wednesday afternoon.

USD

The Dollar dipped 0.2% yesterday, although was little moved following last night’s Presidential debate.

The next major debate will take place on Sunday 9 October, followed by a further debate on Tuesday 19 October. We think both will draw significant attention among currency traders as Election Day begins to approach. The higher percentage of undecided voters in the lead up to this November’s election, around 20% compared to just 12% in 2012, means that the TV debates will undoubtedly take on more importance.

Consumer confidence in the US this afternoon is expected to fall to 99.8 from 101.1. The services PMI will also be worth noting.

Receive these market updates via email

SHARE